now loading...

It all started with an invitation. In early 2005, the former United Nations Secretary-General Kofi Annan invited a group of institutional investors to develop the United Nations Principles for Responsible Investment ( UNPRI ). In 2006, the principles, an initiative to encourage better investment practices, were launched. And, since then, the number of signatories has increased to over 3,000 and the assets under management covered by the principles have reached US$103 trillion.

ESG investing shares similarity with socially responsible investing ( SRI ), but traditionally the stress with ESG has been on the financial relevance of investing and with SRI on the ethics and morals of investing. However, the opinions of Asian local fixed-income investors suggest there may not be that much of a difference.

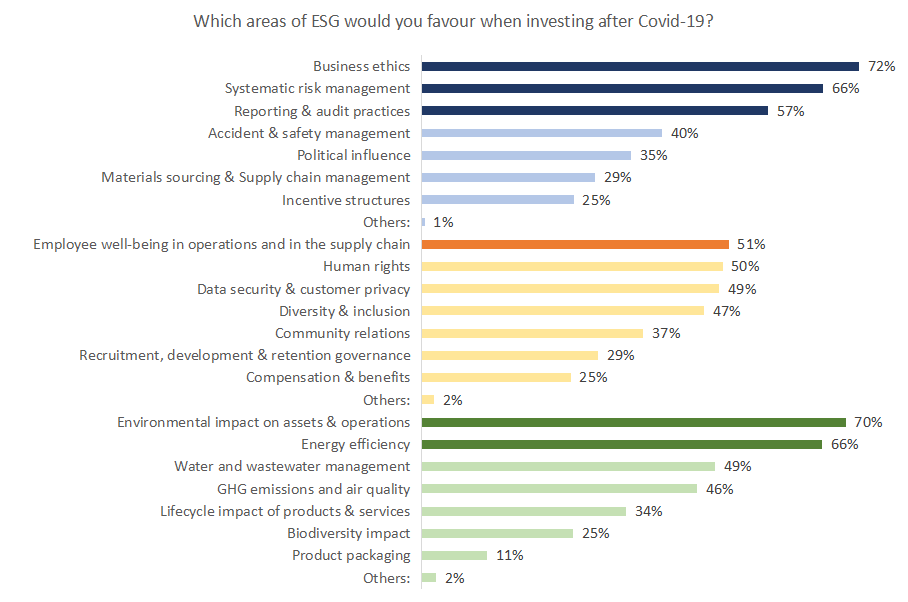

In an Asset Benchmark Research ( ABR ) survey, conducted between 12th June and 2nd July, a 72% majority of the 231 fixed-income investors surveyed for the Asian Local Currency Bond Benchmark Review 2020 picked business ethics as the major ESG area that needs to be focused on since the outbreak of the Covid-19 pandemic.

The other four key areas attracting investors’ attention were the environmental impact on assets and operations ( 70% ), systematic risk management ( 66% ), energy efficiency ( 66% ), and reporting and audit practices ( 57% ). Interestingly, only half of the respondents ( 51% ) picked employee well-being, despite it having become a heated social responsibility topic during the pandemic.

Investors’ slight overweight on business ethics suggests that it is as important as, or slightly more important than, risk management when it comes to long-term investing in Asia.

As an investor managing a shariah-compliant fund suggests: “Most companies should not only serve their shareholders for the main purpose of a corporation; but start serving society, through innovation and commitment to a healthy environment and economic opportunity for all.”

This new finding implies that the financial relevance of business ethics will lead the agenda in terms of future ESG dialogue in the region. However, the intangible nature of business ethics implies that investors will also have to openly share their knowledge more if they are committed to harmonizing ESG standards in Asia.

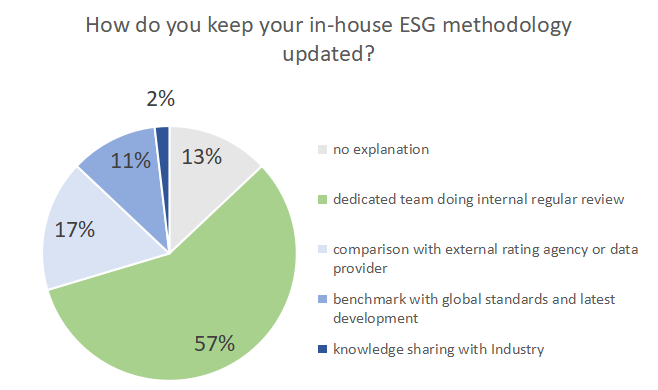

Unfortunately, investors are still working in silos. When asked to explain how they keep their ESG methodology updated, only 2% of local investors recognized knowledge sharing as a way to improve the harmonization of standards. Most of them ( 70% ) either give no explanation or say they have their own dedicated team to conduct annual reviews, without giving specific details of the process.

The survey’s findings demonstrate institutional investors in local markets are convinced of the soundness of their current ESG model, while demonstrating that knowledge sharing among them is still in its early stage of development.

Increasing pressure from asset owners will gradually change the dynamics of this. Japan’s Government Pension Investment Fund, one of the world’s largest, has since 2018 requested that their external managers disclose the details of proxy voting records and submit ESG reports on a regular basis. As well, in 2018, Government Pension Fund Thailand ( GPF Thailand ) set up a 1 billion baht ( US$32 million ) portfolio to invest in 33 listed companies found on the Thailand Sustainability Investment list.

Institutional investors are also earning their ESG investing credentials in Asia. Nearly one-quarter ( 22% ) of surveyed local investors try to differentiate their firms by gaining external recognition, with signing up to international conventions being one of the most popular options.

“We were among the few early ones in Asia and the Indian fixed- income market to sign up to the UNPRI,” notes Abhishek Bisen, fixed-income fund manager at Kotak Mahindra Asset Management, a UNPRI signatory since September 2018.

Yet, when asked to differentiate themselves from their peers, the responses of a large majority of investors ( 78% ) indicated that they were confident in their silos.

“We have one of the largest credit research teams in Asia,” claims a portfolio manager at one of the largest asset management firms in the region. “Every credit analyst within the fixed-income team is well acquainted with the internal ESG evaluation criteria and is responsible for the ESG scoring of issuers under his or her coverage.

“There is arguably no better integration of ESG criteria into the credit analysis than how it is approached by us since the relevant credit analyst rightfully should know his credit best. We, therefore, can evaluate ESG risks in a manner more directly relevant to their impact on credit performance than our competitors.”

Social factors force investor rethink

Despite the investors being confident in their ESG capabilities and commitment, the emerging challenge of social responsibility should spur on investors to the realisation that there is a need for more meaningful engagement and knowledge sharing within the industry.

To illustrate the point, the US Customs and Border Protection, despite the immense need for medical disposable gloves, recently issued a withhold release order on disposable gloves manufactured by the Malaysian firms TG Medical and Top Glove.

The decision regarding Top Glove was made after a media investigation into its factories revealed evidence of migrant worker exploitation that included low wages, excessive overtime, illegal deductions from salaries, extortionate recruitment fees, poor living conditions, and a lack of social distancing arrangements.

In its defence, Top Glove referred to the A rating it received from auditing firm Amfori BSCI as an evidence that its labour practices met international standards. However, Amfori BSCI responded with a press release countering Top Glove’s argument that its rating a priori provides evidence that the manufacturer’s labour practices met international standards.

The Top Glove case demonstrates the pressing need for robust third-party follow-on due diligence on the social aspects of ESG criteria.

“There are limits as to what we can do given our capacity,” states Arsa Indaravijayal, GPF Thailand’s assistant secretary-general. “A comprehensive follow-on after an ESG rating is assigned can be costly, but it is needed to complete the whole ESG process.”

The emergence of third-party certification of ESG factors will, however, give rise to issues related to the proper usage of or over-reliance on external opinion. And, as there is no single solution to the problem of ESG verification, the industry must engage in a constant dialogue with other stakeholders to ensure the ESG framework is being refined.

To view the rankings of the Most Astute Investors in Asian local currency bonds by country, please click here.

To view the rankings of the Top Investment Houses in Asian local currency bonds by country, please click here.

To find out more about Asset Benchmark Research and our Asian Local Currency Bond Benchmark Review, please click here.