now loading...

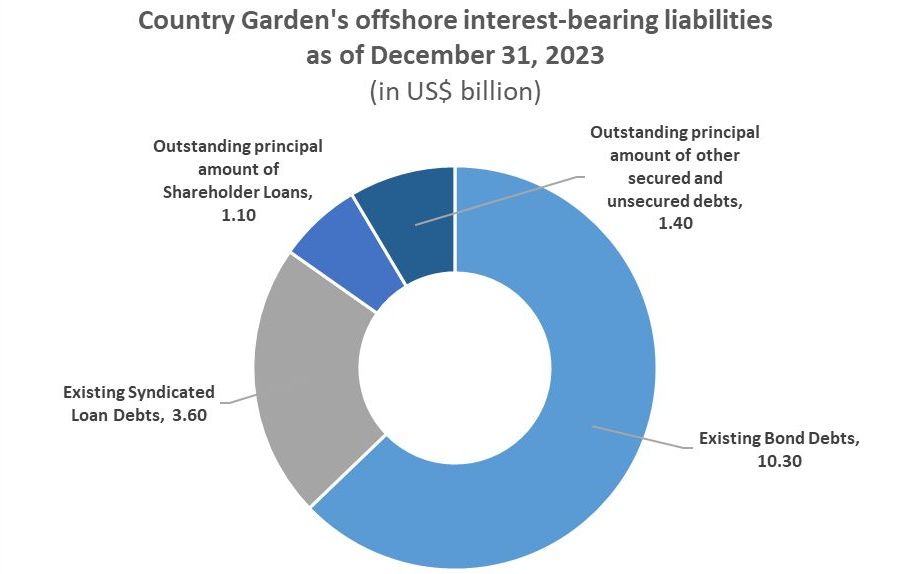

Chinese property developer Country Garden, whose Hong Kong-listed shares are currently suspended from trading, has come up with an offshore debt restructuring plan to deleverage US$11.6 billion of debt from its balance sheet.

In making the move, the company apparently wants to show that negotiations with creditors are ongoing, and to fend off a winding-up petition from investors.

Source: Country Garden

Source: Country GardenAccording to the announcement issued last week, creditors can choose among five debt resolution options that include cash buyback, convertible bonds, and/or new debt instruments.

Creditors can choose the cash payment plan upon the effective date of restructuring, in which they need to accept at least 90% relief on the principal. Or, they can choose to fully equitize their debt holdings through mandatory convertible bonds with a duration of 3.5 years if the restructuring proposal is passed.

In between those two options, they may choose a combination of equitization and debt extension, in which 67% of the amount due will be equitized and the remainder due in 7.5 years.

Finally, investors can choose between a 35% relief on the principal by raising new debt instruments with an extended maturity of 9.5 years, and a no-relief plan with a longer maturity of 11.5 years. The new debt instruments may be repaid through payment-in-kind.

Once a top real estate developer in China, Country Garden has been facing financial challenges since 2022 as the country’s property market stumbled and corporate revenues plummeted. Its interest-bearing debts had mounted to over US$16 billion as of end-2023 and the company started to default on its offshore debt in the same year.

The company owns over 2,900 projects in China. In a positive scenario, based on the assumption that the company keeps its head above water and the property market gradually recovers, these projects are estimated to provide net cash surplus available for offshore distribution in the range of 20-25 billion yuan ( US$2.7-3.4 billion ) from 2024 to 2039.

However, China’s real estate sales continue to slide, although systemic risks in the sector have significantly eased. Latest data from the National Bureau of Statistics shows that sales of new developed residential units from January to November 2024 fell by 22% over the same period in the previous year.

Revitalizing property sales and boosting asset turnover by delivering projects under construction are still the top priorities for Chinese real estate developers.