now loading...

Gold and the US dollar, taken together, are providing investors with a safe haven amid the geopolitical uncertainty and volatility plaguing global markets since the beginning of the year.

Although it is only two weeks into 2025, financial markets have exhibited notable volatility, influenced by various economic indicators and policy uncertainties including inflation concerns, unusual bond market movements, and the changing of the guard in Washington.

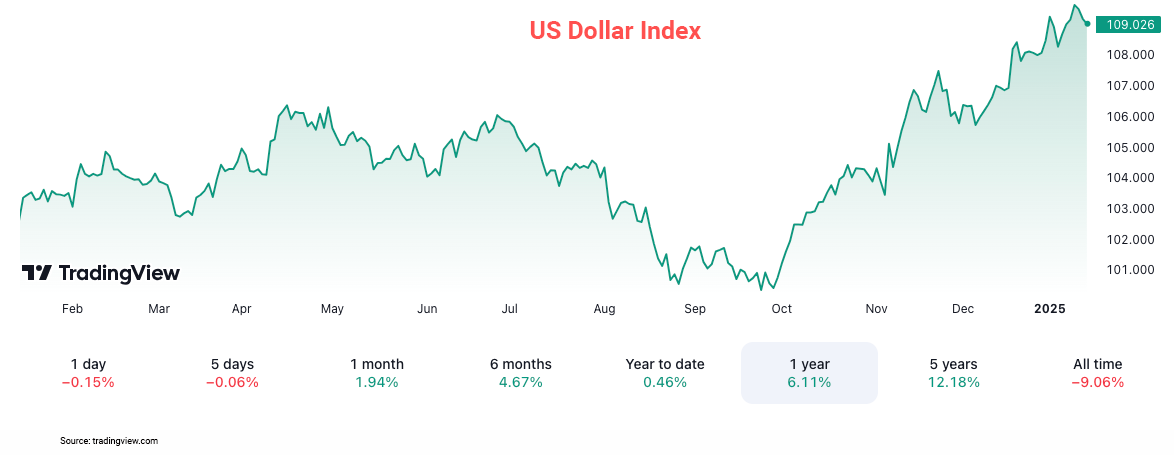

Meanwhile, the US dollar has strengthened since January 1, reaching multi-year highs, influenced by robust economic indicators and shifting monetary policy expectations. The US Dollar Index ( DXY ), which measures the dollar against a basket of major currencies, reached a two-year high on January 2. As of January 15, the DXY stood at 109.026, down from 109.27 the previous day.

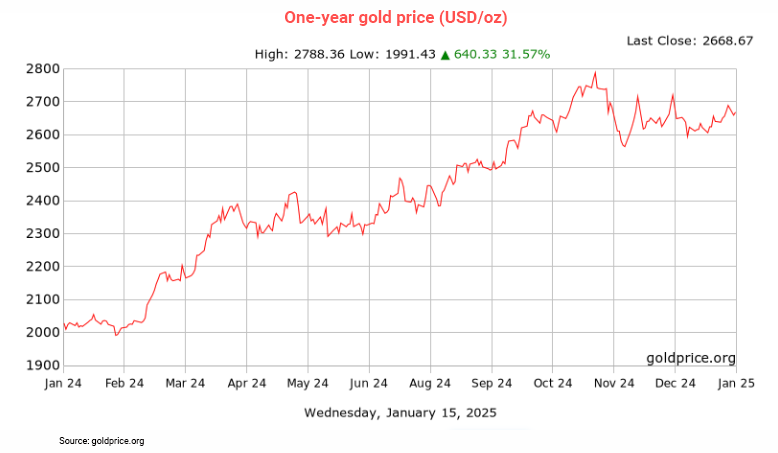

Gold, on the other hand, has remained relatively stable with a slight upward trend despite external economic pressures. As of January 15, the gold price was US$2,668.67 per ounce, indicating a slight increase from US$2,623.96 at the start of the year.

While gold and the US dollar traditionally have an inverse relationship – when the dollar strengthens, gold prices decline, and vice versa – the fact that both have been on an upward trend since the beginning of the year indicates that investors are flocking to these asset classes away from riskier ones.

Explaining the trend, market experts note that the complementary characteristics of gold and the US dollar make them good core assets for a diversified safe-haven strategy. While gold is a hedge against inflation and currency devaluation, the US dollar remains a liquid and universally accepted currency.

Consider risk factor

“We do anticipate that the US dollar is likely to remain stronger for longer. It also continues to be a safe haven in markets with any geopolitical uncertainty and volatility,” says Michele Barlow, Asia-Pacific head of investment strategy and research at State Street Global Advisors.

Barlow, however, cautions longer-term investors that the US dollar may already be overvalued by 10%-15%, a risk factor that has to be taken into account for long-term portfolio construction.

Gold, on the other hand, may experience a price consolidation in 2025 depending on economic indicators, interest rate movements, as well as supply and demand dynamics, particularly purchases by Asian central banks.

The US Federal Reserve’s monetary policy of controlling inflation is keeping interest rates higher for longer and higher interest rates generally make non-interest-bearing assets like gold less attractive, potentially leading to price consolidation or even decline.

According to a report by VT Markets, historical trends indicate that gold prices typically peak within two quarters of a rate cut cycle. It predicts that gold will maintain its upward momentum through early 2025, though its annual growth may taper as markets absorb the impact of monetary easing.

However, gold remains a critical asset in diversified investment strategies, particularly in an uncertain economic environment.