now loading...

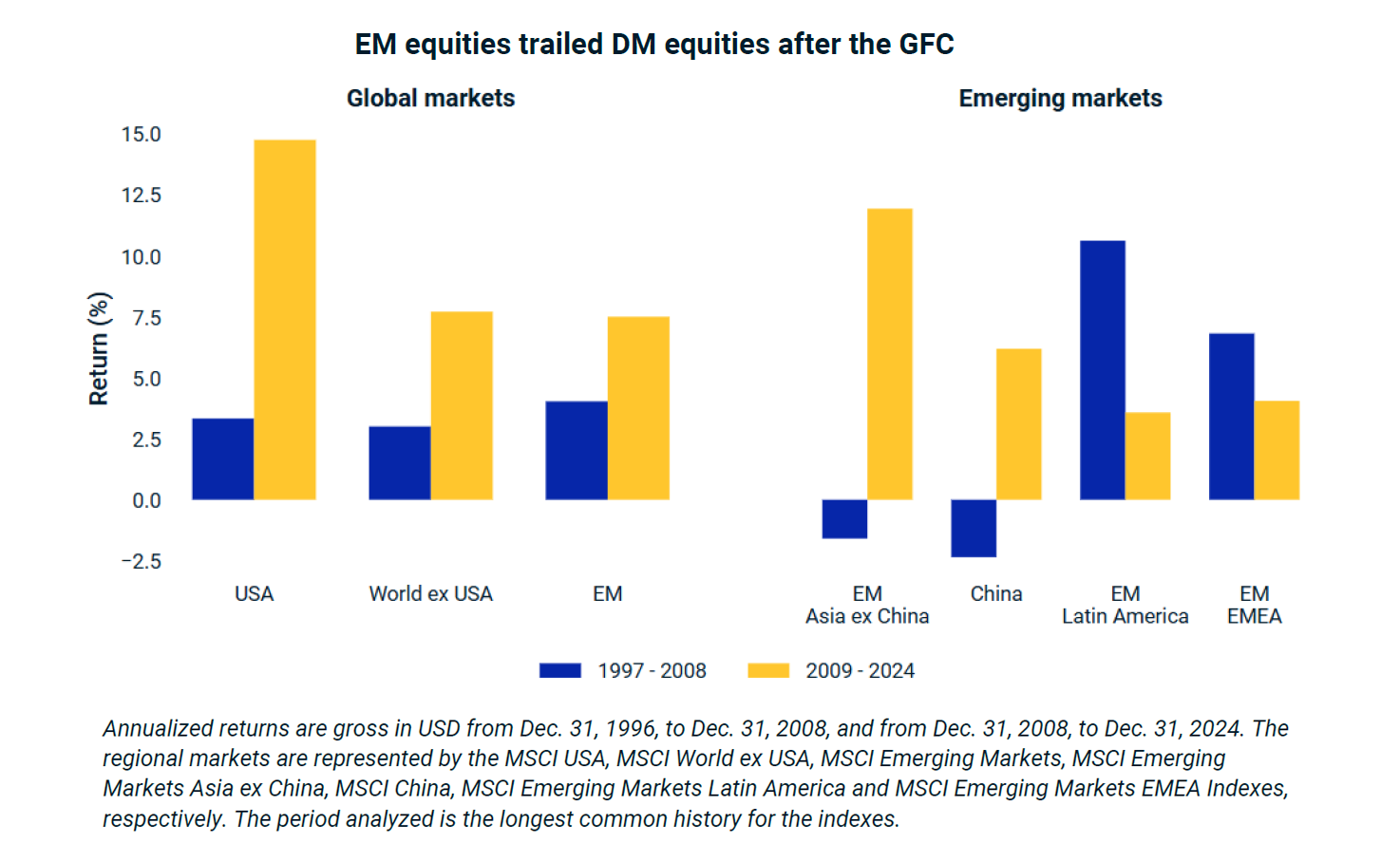

Since the 2008 global financial crisis, emerging market ( EM ) equities have underperformed their developed market ( DM ) counterparts by almost 5% annually, prompting investors to reassess the role of EM in their equity allocations. This underperformance is in stark contrast to the burgeoning growth of EM economies, according to a new report.

The number of EM securities has doubled since 1998. But while the rise in trading activities has fuelled positive investor sentiment, the growth in market capitalization has been slow, MSCI says in its latest analysis, Long-Term Investing in Emerging Markets – Identifying Drivers of Total Shareholder Return in Emerging-Market Equities.

Emerging markets have grown 8.7% in aggregate earnings over the last 20 years, but this strong momentum has not fed into the stock markets. In addition to weakened currency curbing corporate earnings, investor confidence has been dented by diluted share values resulting from the rise of equity financing activities, including secondary offerings.

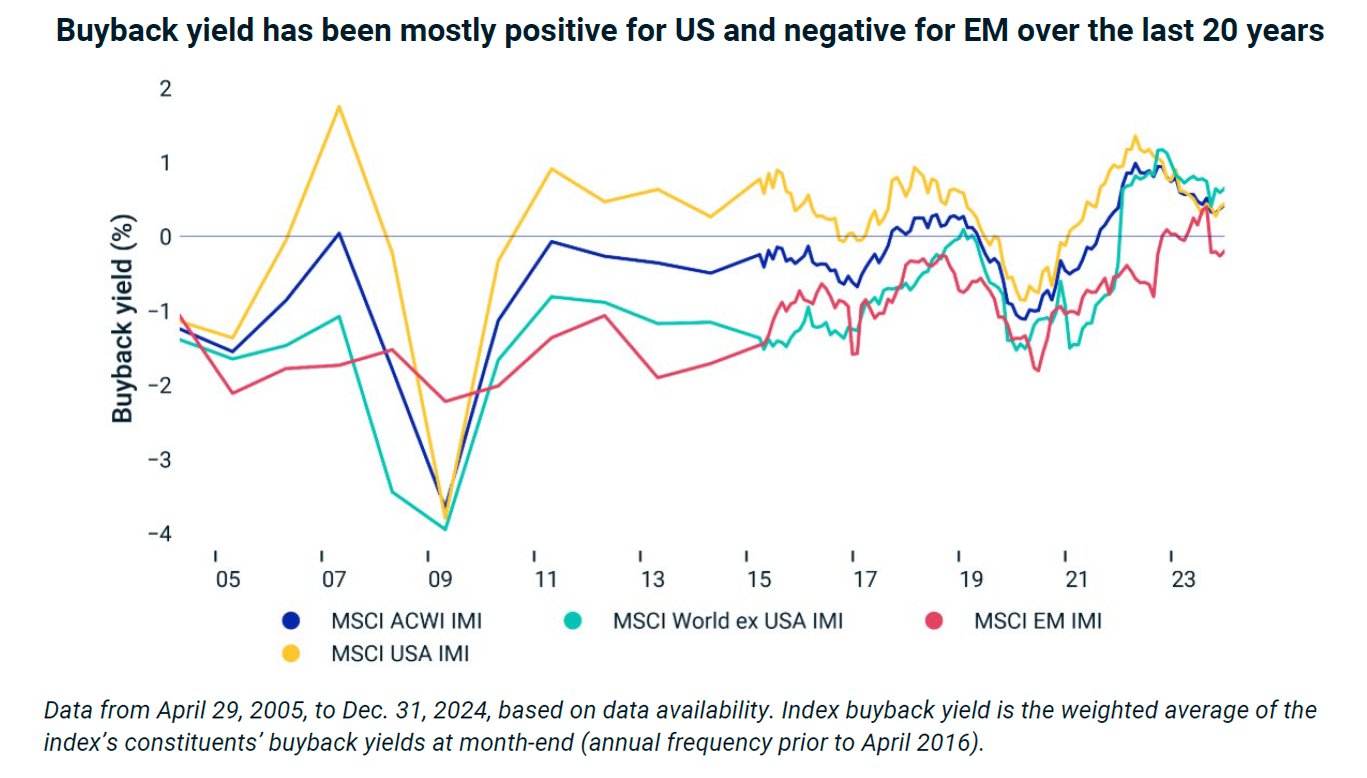

Compared to frequent buybacks in the US equity market, buyback yields in emerging markets were negative between 2005 and 2023, amid a strong flow of new listings and share issuance. The new shares also curtailed the dividends and earnings of investors.

In emerging markets excluding China, earnings per share ( EPS ) grew 5.6%, compared to 9% in the United States. Despite their healthy fundamentals, EM stock markets lost their sheen under narrowed valuation metrics.

In the course of gaining familiarity with EM stock markets, investors often struggle with garnering relevant information due to limited analyst coverage. While more analysts need to come forward to support market research, the report stresses that it’s equally important for them to broaden the scope of their exposure, for instance, from corporate-specific risks to such aspects as country, currency and industry, which will be useful to enhance accuracy.

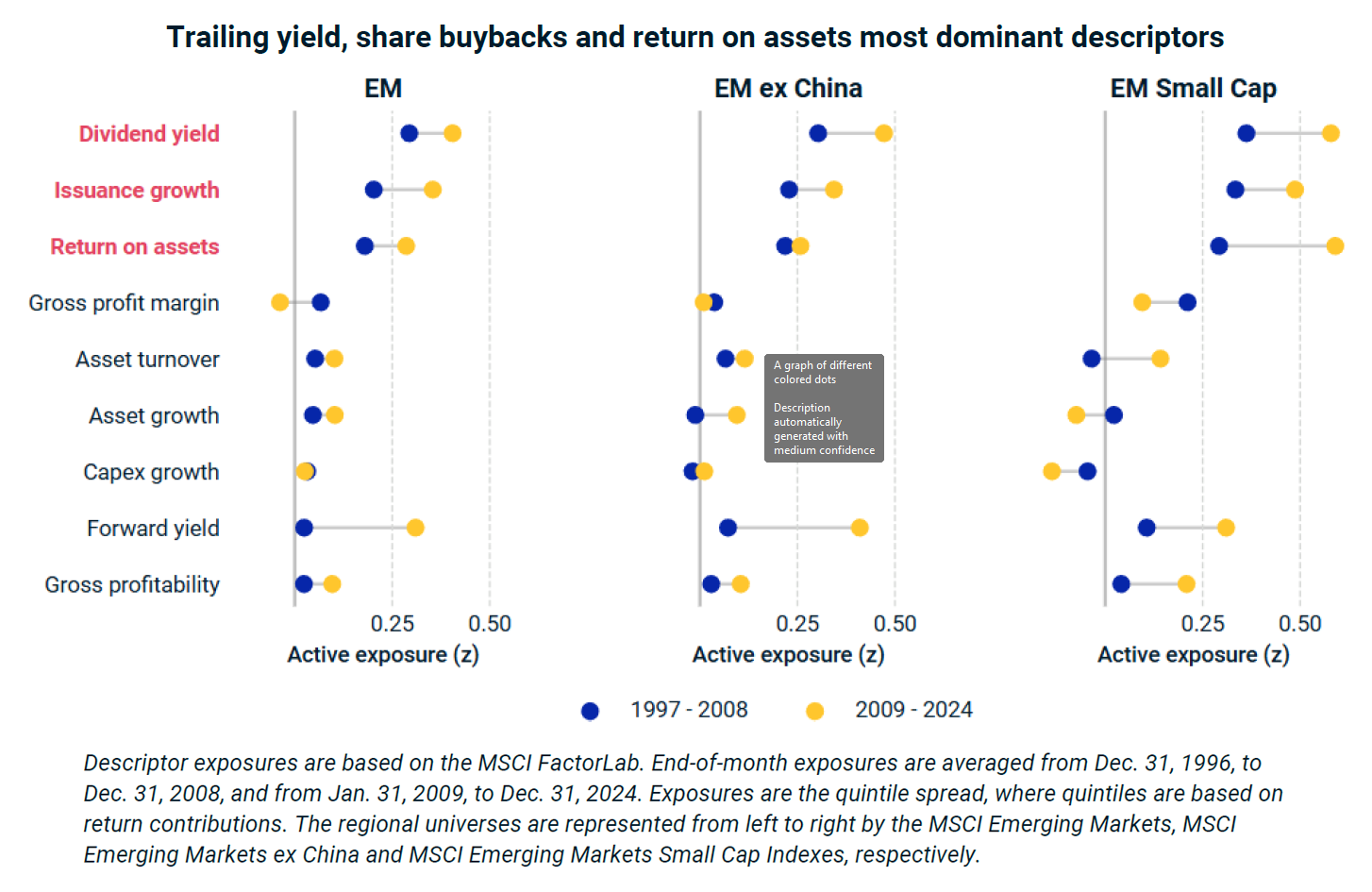

From growth to profitability

Top EM players are characterized by their definitive roles in navigating market performance. Almost all of the EM returns are delivered by the top 20% stocks, compared to 80% in their developed counterparts.

“Winner-takes-most dynamics often appear in fast-scaling industries such as technology or internet platforms,” says the report. “In EM, these effects can be even more pronounced, with a handful of companies – sometimes state-backed with policy support – capturing outsized advantages.”

These long-term strong gainers, also known as compounders, don’t necessarily appeal to the market with robust growth, but more often to those with business stability and operation consistency, which are manifested in factors such as higher dividend yield, share buybacks, earning stability, and profitability.

In contrast, high-growth stocks are identified with weaker dividends and higher earnings volatility. Almost half of the top-growth stocks fell out of the rank in a year, but those stable gainers retain top rankings for more than five years.

“Even as [the compounders’] topline growth moderated, their ability to maintain margins allowed them to preserve earnings power – and ultimately drive total return,” the report says.

Brushing off the headwinds of weak currency and share dilution, emerging markets offer opportunities in corporates with less growth but strong fundamentals, those that offer disciplined returns and dividend yields, presenting investment opportunities amid a fickle market.