now loading...

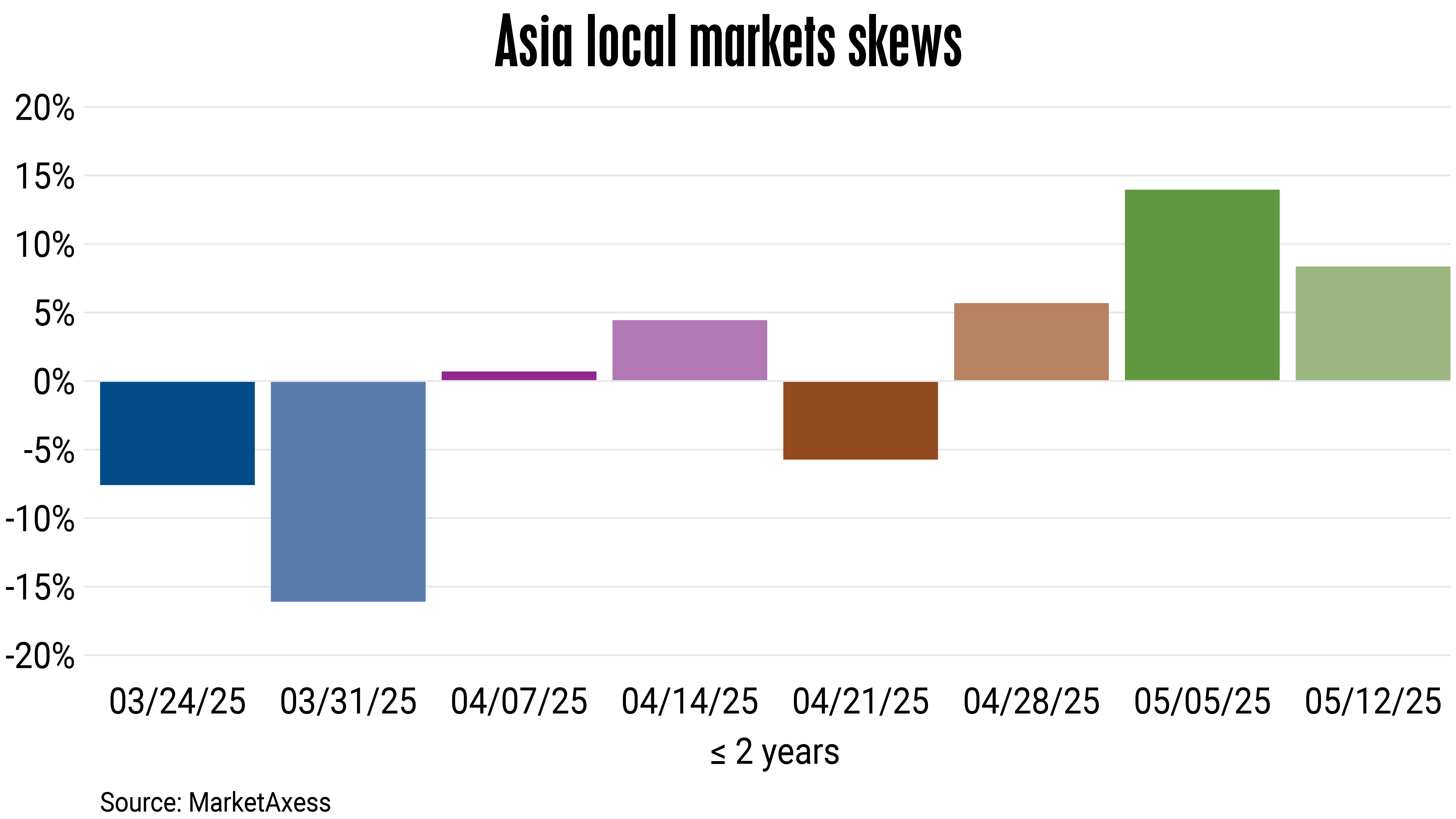

Investor sentiment in short-dated Asian local currency ( LCY ) bond markets has moved from a deep negative to a strong positive skew in just a few weeks from late March to early May, suggesting a major shift in market expectations.

This trend, as can be gleaned from LCY bond trading data from MarketAxess, a regional fixed income trading platform, is driven by several factors, including monetary easing by Asian central banks, improved FX outlook of Asian currencies as a result of the weaker US dollar, and perceptions of reduced geopolitical and trade uncertainties.

In bond markets, “skew” refers to the steepness or flatness of the yield curve, deviations in yields or pricing differentials between local markets and benchmarks like US treasuries or swaps, and/or risk premiums demanded by investors, possibly driven by macro conditions like tariffs, FX risk, or central bank policy.

“The progression from deeply negative to strongly positive skews over six weeks indicates a repricing of short-term risk,” says Roheet Shah, head of Hong Kong and head of dealer sales, Asia-Pacific, at MarketAxess in an interview with The Asset. “This is in and around the story of inflation, central bank policy expectations, and the weaker dollar. In markets, if you have a dovish central bank or dovish central bank policy expectations and a weaker dollar, investors typically tend to focus on the very front end of the curve.”

Shifting market sentiment

In late March to early April 2025, trading data ( see chart ) shows negative skews in short-term tenors, particularly two-year maturities, implying that short-dated local bonds were under pressure possibly due to rising inflation fears, rate hike expectations, FX depreciation, or capital outflows.

This period coincided with US President Donald Trump’s tariff escalation, which stoked fears of inflation and monetary tightening. This, in turn, resulted in a bearish investor sentiment on short-term Asian LCY bonds; investors demanded high risk premiums, driving short-dated yields higher.

By mid to late April, the skews start turning positive or neutral, suggesting that market sentiment had stabilized, with less demand for risk premium. Investors were still cautious but less bearish compared to the period from late March to early April.

Around this time, Asian central banks began cutting interest rates or signalled dovish monetary policies. The People’s Bank of China cut the one-year loan prime rate by 10 basis points on April 21, and the Reserve Bank of India cut its benchmark repo rate by 25bp on April 9. The Reserve Bank of Australia, although it did not cut interest rates in April, implemented a 25bp rate cut on May 20.

By May, the skews have turned sharply positive, rising up to around 15%, indicating increased demand for short-term local bonds, amid easing policy expectations, currency stabilization, and stronger risk sentiment, possibly tied to a weaker US dollar, which boosted the appeal of Asia LCY bonds.

The sharp turnaround reflects a more positive investor sentiment as the greenback continued to weaken, extending the losses experienced earlier in the year. The US dollar has depreciated by over 8% by mid-May, following a 4.6% decline in April.

Rate cut expectations

Also, announcements from the US Federal Reserve fuelled broad expectations of rate cuts later in the year. There were significant foreign inflows into Asian LCY bonds, particularly in South Korea, India, Malaysia, and Indonesia.

Even amid the heightened global macroeconomic uncertainty, MarketAxess data indicates strong and sustained buying across most Asian local fixed income markets, with aggregate net better buying consistently exceeding 74% in the first week of May alone.

Singaporean and Malaysian government securities saw strong net better buying across all three days ( May 5-7 ), driven primarily by demand at the very front end of the curve. Philippine local government bonds also attracted high net buying interest across the full maturity spectrum during the period.

Meanwhile, amid the recent hostilities between India and Pakistan, MarketAxess observed healthy two-way flows on the front end, with a stronger bias towards net selling. The front end also accounted for a significant share of overall trading volumes in Pakistan.